New Delhi: October has been a better month for the Indian two-wheeler segment as indicated by the latest data released by the Society of Indian Automobile Manufacturers (SIAM). It is expected to get a further boost as the festive season extends to mid-November.

In October 2020 total domestic sales of two-wheelers increased 16.88% to 20,53,814 units as against 17,57,180 units in the same month last year. Two-wheeler production also jumped 40.14% to 24,18,028 units in October 2020 from 17,25,462 units in October 2019, reflecting the robust demand.

Motorcycle sales for the month were at 1,382,749 units as against 1,116,886 units in October 2019, up 23.80%, while scooter sales saw only a marginal growth of 1.79% to 590,507 units as against 580,120 units in the same month last year.

| OEM | YTD FY’21 (April-Oct) Market Share (in %) | YTD FY’20 (April-Oct)Market Share (in %) | Change (in %) |

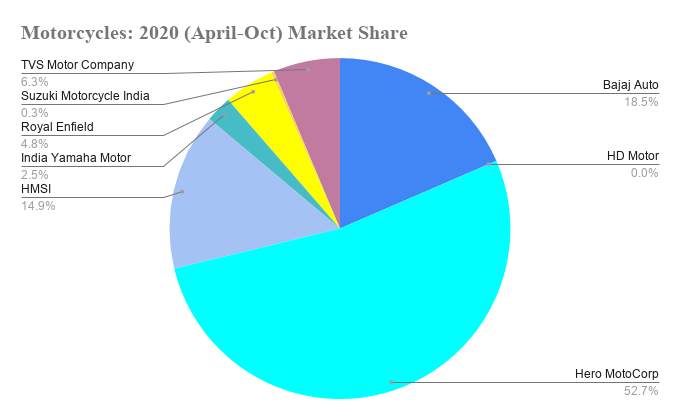

| Bajaj Auto | 13.1 | 12.5 | 0.6 |

| Hero MotoCorp | 40.4 | 36.6 | 3.8 |

| HMSI | 25.9 | 28.8 | -2.9 |

| India Yamaha Motor | 3.6 | 3.4 | 0.2 |

| Royal Enfield | 3.4 | 3.6 | -0.2 |

| Suzuki Motorcycle | 3.2 | 3.9 | -0.7 |

| TVS | 10.5 | 11.3 | -0.8 |

Source: SIAM

While the urban markets are still grappling with a rising number of COVID-19 cases, the comparatively less impacted rural and semi-urban markets have enabled a sequential improvement in sales. In August and September 2020, the industry recorded 22% and 19% sequential growth and a Y-o-Y 3% and 12% growth in wholesale volumes, respectively.

Japanese companies lose ground to Indian counterparts

Another notable factor has been the changing dynamics of market share in the two-wheeler segment amidst the COVID-19 pandemic during which Japanese automakers have ceded their share to Indian counterparts.

The segment leader and the world’s largest two-wheeler manufacturer Hero MotoCorp further strengthened its position and increased its market share to 40.4% in FY20-21 in comparison with 36.6% a year ago. Whereas, the Japanese automaker Honda Motorcycle and Scooter India (HMSI) lost its India share by 3% to 25.9% so far in this period.

Meanwhile, the share of Japanese companies declined to 32.7% from 36% last year. Deep penetration in rural markets and a large portfolio of entry-level offerings have helped Indian companies to gain market share at the expense of the Japanese firms. It remains to be seen if this is just a Corona virus-induced phenomenon or going to continue in the long run.

The entry-level motorcycle space is dominated by Hero MotoCorp. In fact, Hero claimed that October 2020 sales numbers are its highest-ever in any single month. The company posted a growth of 35% to 806,848 units owing to a positive turnaround in customer sentiments, particularly for motorcycles across markets.

The first-time buyers in rural areas have been the biggest drivers of growth in this segment, and according to Hero, the demand was such for the entry-level two-wheelers that ramping up supply became a concern.

In the 125-150 cc segment, Bajaj Auto has been the biggest gainer recording an increase of 12%.

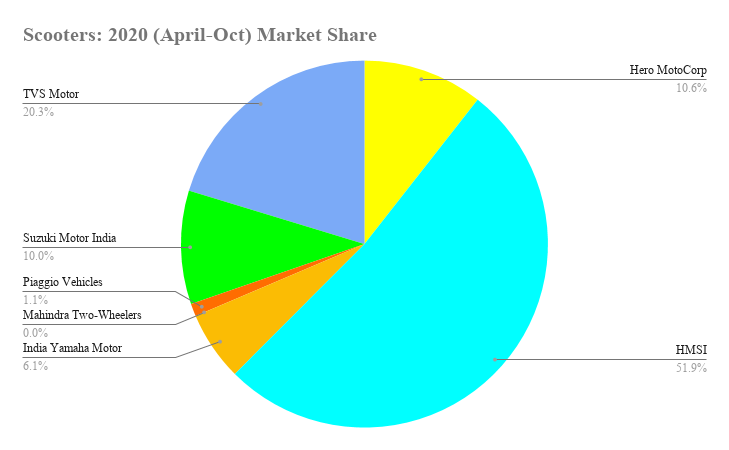

In the scooter space, the market leader HMSI maintained its pole position commanding over 50% of the market. However, it lost its market share by 4% in FY21 as compared to the last fiscal year, which resulted in a gain for Hero MotoCorp and TVS Motor.

Premium motorcycle segment heating up

In the premium segment, competition is increasing with mass motorcycle manufacturers planning to foray into that space. Royal Enfield has been commanding the premium segment, but now more competitors are planning launches in this space to capture the urban market.

HMSI entered in the middleweight motorcycle segment – 300cc and above – with the launch of Highness CB 350. It will be a challenge to the likes of Royal Enfield Classic 350, and Jawa in the premium bike segment.

Earlier Hero MotoCorp’s chairman, managing director and CEO Pawan Munjal had told ETAuto that it would be making strides into the big bike segment as it graduates into heftier and sporty machines that would be ideal for the millennials and also would meet its appetite to enter the developed markets.

With competition becoming more intense, Royal Enfield is also beefing up with an aggressive product strategy to protect its turf. The company has over 15-20 product actions under consideration for the coming three to five years.

Bajaj Auto, which drives a large chunk of its sales from the premium segment, has constantly been losing its market share for want of new launches. The company has restricted itself mostly to refreshers of its earlier models.

Meanwhile, Bajaj has also partnered with Triumph to manufacture 300-700 cc motorcycles which are expected to hit the market in 2021.

Outlook for FY21

Despite the strong performance, the segment will see a volume contraction of 16-18% in FY21 as compared to FY20, according to ICRA.

Earlier the rating agency had projected two-wheeler sales to decline by 11-13% in the current fiscal. The revised outlook comes in line with the overall macroeconomic scenario, the COVID-19 demand-supply disruptions, looming income uncertainties and increased cost of ownership of BS-VI vehicles.

However, the two-wheeler OEMs will continue to have strong credit profiles characterised by healthy return on capital employed (ROCE) — average ranging between 18% and 20% — and comfortable balance sheets with negligible debt and strong cash and liquid investments, the rating agency said.

In the urban markets, which continue to be severely impacted by repeated waves of COVID-19, a preference towards personal mobility could push near-term two-wheeler demand. However, these would only help to partially offset the adverse impact of the pandemic.

On the export front, while the long-term drivers remain favourable, the fall out of COVID-19, and volatility in the crude oil price which impacts demand in key markets, remain a near-term negative.

{kind=link}